Philippines: Stagflation Purgatory

Image source: “NEDA Building Photo” by Rpangeles

Stagflation: A Once-in-a-Blue-Moon Disaster

Stagflation is defined as a phenomenon in economics wherein a country’s GDP growth rate is slow amidst a swift inflation of prices of goods. Theoretically, this is should be improbable, and quite paradoxical. The timeless Philipps curve, wherein inflation is shown to be inversely correlated with GDP growth rate, testifies to the apparent incompatibility of economic growth slowdown and high inflation.

However, this has already happened in the United States of America in the 1970s. The cost of stagflation for the Americans was high and it took a lot of political and economic sacrifice for it to be solved in ten years.

This is a particular problem as stagflation seems to be starting in the Philippines. Stagflation is a looming problem and it is threatening to destroy the livelihoods of Millions of Filipinos.

With that being said, we shall now discuss how the Philippines ended up in this situation in the first place.

Ice-Cold Inflation

Inflation refers to the phenomenon in an economy where prices of goods and services rise. Inflation is measured by calculating the weighted average percentage increase in the price of goods in a “basket of goods” containing products and services that economists deem to be representative of the typical goods and services purchased by the average citizen in a specific jurisdiction at a given period of time. There are two kinds of inflation metrics: headline inflation and core inflation. To simplify the discussion, “inflation” here refers to headline inflation. While I acknowledge the importance of core inflation, discussing it is beyond the limitations of this article.

To talk about the historicity of inflation rate in the past five years is necessary to give context to the inflation rates seen up until 2025.

The years 2020 and 2021 were a remarkably turbulent and memorable time for Filipinos as this is when the COVID-19 global pandemic hit the Philippines the hardest. The pandemic had a myriad of adverse effects to the lives of Filipinos. Notable damage of the pandemic can be seen in the economic health of the country. During the pandemic, the GDP of the Philippines contracted, and unemployment rates hit double-digit percentages.

As a response, the Bangko Sentral ng Pilipinas (BSP) and the rest of the government conducted monetary and fiscal policy measures to stimulate the economy and lessen the economic damage brought about by the pandemic.

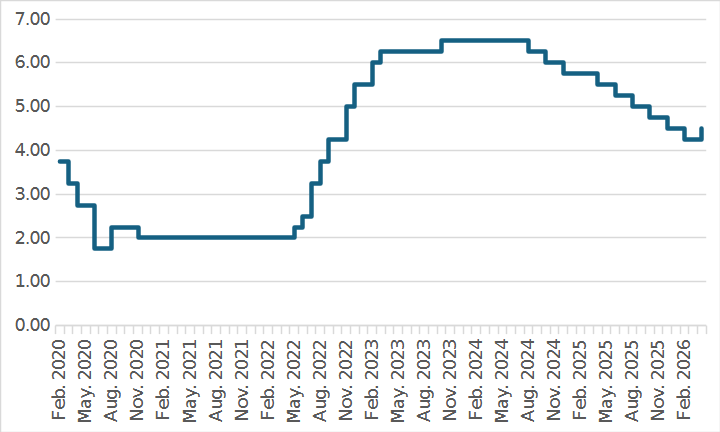

In terms of monetary policy, the BSP cut its overnight repurchase facility interest rate by up to 175 basis points (bps) from March 2020 to December 2020. The BSP also injected P300 billion through quantitative easing.1 Both initiatives were done in the hope of lowering bond yield rates, and bring the cost of capital down.

Chart A: BSP policy rate (2020-2026)

In terms of fiscal policy, the Philippine government gave out stimulus checks or “ayuda” to Filipino families. According to the Department of Interior and Local Government (DILG), the total amount of ayuda distributed during the pandemic was worth PHP16.29 billion in just the National Capital Region (NCR), Bulacan, Rizal, Laguna, and Cavite.2

In hindsight, the consensus among analysts seems to be that the policies initiated by BSP and the government were able to mitigate a bulk of the economic damage of the pandemic.

A key takeaway that all economists get from Economics 101 class is that everything has a trade-off. What could be the trade-off of all this? The Philippine economy was saved. But at what cost?

The cost of these monetary and fiscal policies came as rising inflation in 2022 and 2023. See chart A below as reference.

Chart B: Philippine Inflation Rate (2020-2026)

In those particular years, inflation was red hot. Headline inflation prints during this period topped out at almost 9.00 percent. The reason for this? Pent-up demand. Coming out of the pandemic, people had pent-up demand to consume. A lot of free money and cheap money (due to the low cost of debt) was injected into the financial system because of the monetary and fiscal policies during the pandemic. The price that our society paid, so that our economy could be saved, was red-hot inflation. That was the trade-off.

Due to the high inflation in 2022 and 2023, the BSP responded by hiking policy rates throughout this period as seen in Chart A. To say that the BSP simply hiked the policy rates is an understatement because the hike was so steep. In fact, by the end of the hiking cycle, the BSP policy rate topped out to 6.25 percent, which is a 450-bp increase from the pandemic-level low of 2.00 percent in December 2020. If we compare this to the pre-pandemic level of 3.75 percent, the difference is 275 bps.

I remember back then that there were speculations of an economic “crash landing” due to the seemingly “steep” and “drastic” policy rate hikes. There were talks that the BSP “jumped the gun” per se. The question in everyone’s mind back then was this: “Did the central bank overdo it?”

The inflation rate from 2024 to 2025 seems to support the idea that the central bank did indeed “jump the gun” and overdid the policy rate hikes. Look at Chart B again. An important detail here is that starting December 2023, inflation was finally back within the prescribed and “manageable” 2.00-4.00 percent band set by the BSP. However, by March 2025, the inflation print came out at 1.75 percent, and consistently continued to be below 2.00 percent until December 2025, with the lowest being 0.95 percent in July 2025.

Now, many, especially those with no training in economic analysis, would say that zero or near-zero inflation is good for the economy. After all, if there is zero inflation, then that means prices of goods did not increase and the buying power of money remain unchanged. Using the same logic, it can be argued that deflation, or the phenomenon where the inflation rate is negative, meaning the prices of goods decreased, would be best for the economy.

I urge those who think this way to stop this faulty way of reasoning. Low inflation and deflation are not good for the economy because these often imply a slow economic growth.

To make this more intuitive, think of it this way: in an auction, the price of the item goes up when interested buyers bid up the price. The more people there are that want that item, the higher the price goes up. In the same way, that is how it is in the economy. Prices for goods go up because there is more demand for it. People compete to have the goods by offering higher prices than other people.

Using this logic, it can now be demonstrated how low inflation implies slow economic growth. When the inflation rate is low, this means that the demand for goods is decreasing. While there are many reasons to explain this decrease in demand, I believe that the reason for this in our present situation is because of the rise in unemployment (which I shall discuss in a later section). When people become unemployed, they lose income. When people no longer have an income, they are unable to demand to purchase many goods that they would have otherwise demanded to purchase had they had an income.

Before I go any further, I acknowledge that some readers might attack what I just said by saying that the change in demand is the sole reason why inflation fluctuates. Indeed, I agree with this sentiment. Fluctuations in the supply side of the economy can also cause inflation fluctuations. However, in the case of the situation I am trying to describe here, I believe that the fluctuations in inflation rate prior to the Iran War and starting in 2024 was mostly, if not solely, due to changes in demand levels. I cannot recall a major event within this time that resulted in supply disruptions or increase thereof.

Anyway, the point I am making here is that low inflation rates prior to the Iran War imply Philippine economic growth has slowed down. I will therefore discuss our anemic GDP growth in the next section to substantiate this claim.

Anemic GDP Growth

The GDP is the primary economic indicator used to measure the economic growth of a country. GDP is the monetary value of all the final goods and services produced within the borders of a country at a specific period. There are two kinds of GDP measures: nominal, and real GDP. To simplify the discussion, any reference to the word “GDP” in this article refers to real GDP. I deem it to be more meaningful, as it removes the influence of inflation, giving a more accurate picture of the economic productivity of an economy.

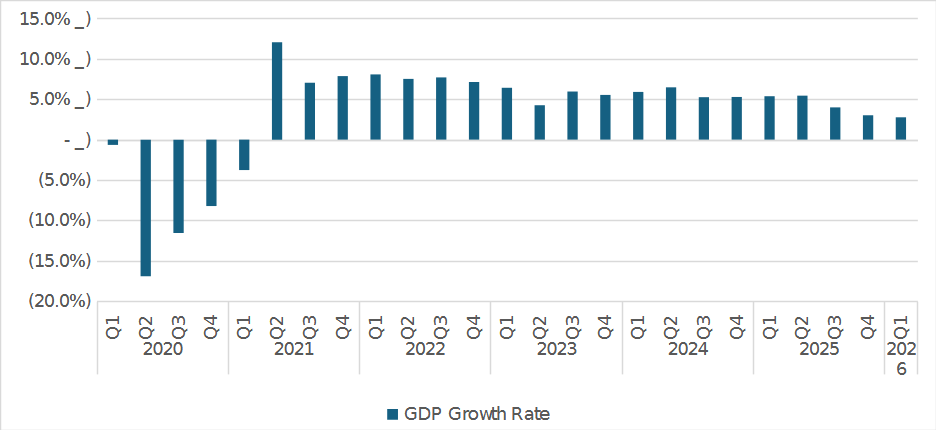

Chart C: Philippine GDP Growth Rate (2020-2026)

Shown in Chart C above is the quarterly GDP growth rate of the Philippines from 2020 to 2026. Looking at the chart, the GDP growth rate data seems to support the idea that the monetary policy rate hikes in 2022 and 2023 were too excessive. It is said that the effect of policy rate decisions can take months before becoming actualized in the economy.

Interestingly, after the BSP finished its rate hiking cycle in August 2024, the GDP growth rate started slowing down. Starting in the third quarter of 2024, the GDP growth rate struggled to hit a 6.00 percent annual growth rate, a rate that was historically hit with relative ease in the pre-pandemic period.

The pattern is clear here: as the effect of policy rate hikes in 2022 and 2023 started trickling down into every fiber of the economy, the economic growth of the Philippines also slowed down. And as of writing this article, the latest GDP growth rate is 2.80 percent as of Q1 2026, which is way below the 5.00-6.00 percent target set by the government and the 3.40 percent median estimate by private sector economists.3

Some readers who are not familiar with economic analysis might not be aware how an increase to central bank policy rates can slow down an economy. To keep it short, rising policy rates make interest rates higher. When interest rates are higher, the cost of both debt and equity capital becomes higher as well. And when the cost of capital is high, many investments become unprofitable. Because these investments become unprofitable, people no longer undertake them. And when people no longer undertake some investment opportunities, job creation is slowed, cost of operating businesses become more expensive, and as a result, consumption is slowed.

Rising Unemployment Rate

Unemployment rate measures the percentage of the total labor force that is unemployed at a given period. A higher unemployment rate means that a higher proportion of the labor force is unemployed. In theory, a higher unemployment rate is a negative indication for an economy.

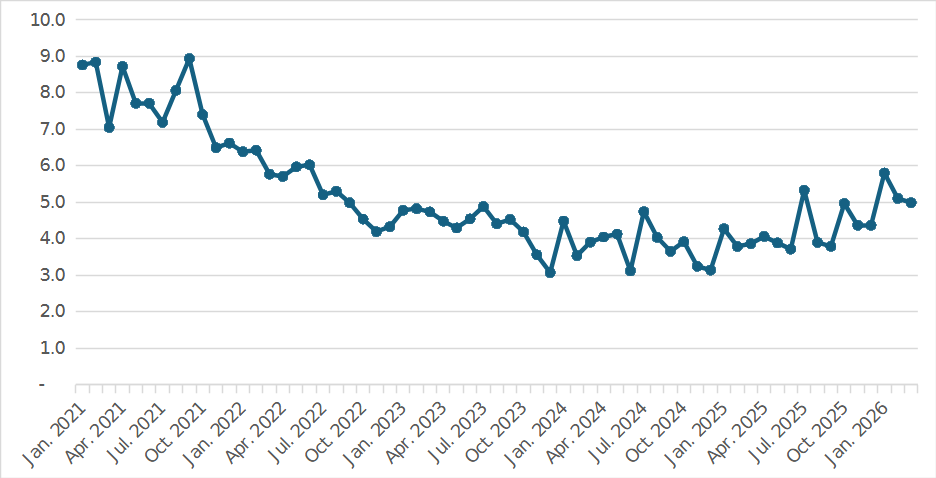

Chart D: Philippine Unemployment Rate (2021-2026)

Chart D above shows the unemployment rate of the Philippines from January 2021 to March 2026. A trend that can be seen here is that the unemployment rate has risen from 3.10 percent in December 2023 to 5.80 percent in January 2026. This is a worrying trend. If anything, this is consistent with the declining GDP levels.

The Specter of Stagflation Looming over the Philippines

Thus far, I have analyzed the Philippine economy without making a mention of the conflict in Iran. This is intentional. I wanted to show that there are reasons to believe that even without the impact of the conflict in Iran, the Philippines’ economic growth is faltering. Personally, I dare to say that the country is on the path towards a recession.

But it is necessary to consider the effect of the conflict to get a full picture of the state of the Philippine economy today. The Philippines has started to once again enter a high inflation period. As of April 2026, the headline inflation print is at 7.70 percent. This is expected to get worse as inflation expectations shift upwards amidst the uncertain situation in Iran.

Assuming my hypothesis that Philippine economic growth is faltering, then combining that with high inflation implies that the Philippines is entering a stagflation era. This is the worst situation that a country can ever find itself. This situation introduces a dilemma to the central bank.

Monetary Policy Decisions Moving Forward

The BSP must choose between economic growth and price stability. While I do not want to make any predictions about what will happen next, I know for sure that the BSP is facing a dilemma. The BSP must either cut or hike policy rates in the next meeting. Whatever choice will be made has an immense consequence.

Should the BSP choose to prioritize price stability, then it must hike rates. However, hiking the policy rate will further slow down the economy, and may very well push the country to an economic recession.

If the BSP chooses to prioritize economic growth instead, then the policy rate must be cut. However, hiking the policy rate will very likely make inflation worse, which will have immense adverse effects to the buying power of the Peso. This could easily destroy livelihoods. Anyone remember the situation of the Weimar Republic in the early 1900s? Too harsh?! Well, how about the USA in the 1970s?

How About Fiscal Policy?

Fiscal policy is a tricky suggestion for the situation of the Philippines. Theoretically, fiscal policy is generally inflationary. Fiscal policy is a direct injection of capital into the economy by the government. Fiscal policy will mitigate the slowdown of economic growth. However, in exchange, this will worsen inflation.

A Lesson from the Past: The 1970s United States Stagflation

Although rare, stagflation is not something that has never happened before. In the 1970s, the United States of America experienced stagflation. Inflation in the USA peaked at 13.39 percent in 1979 with only 3.20 percent GDP growth.

Eventually, the USA was able to break stagflation. How did they do it? The U.S. government had to choose between solving high inflation first or anemic economic growth. The US government chose the former and once that was done, the latter was then addressed.

However, this took ten years. Further, the Federal Reserve had to implement a steep policy rate hike that reached up to 20.00 percent resulting in 10.00 percent unemployment rate. Furthermore, Chairman Paul Volcker had to work overtime to convince the people that the Federal Reserve can curb inflation. These actions settled inflation expectations, preventing inflation from continuing to speed up.

After fixing the inflation problem, the government conducted fundamental reforms to stimulate the economy. These reforms included deregulation and corporate tax cuts.

I feel that should an inflation truly happen in the Philippines, the same must be done.

The Silver Lining

It is hard to find any silver lining in this situation. The only silver lining that can be found are the investment opportunities that this presents. A recession will present an amazing opportunity for people to invest in good quality assets as their valuations drop because of the recession or economic stagnation. Once the economy finally recovers, these assets will then appreciate, making the investor’s wealth increase by a huge magnitude.

But what use is a silver lining if it benefits one man at the expense of another?

1 https://www.bsp.gov.ph/Pages/ABOUT%20THE%20BANK/Events/By%20Year/2023/Research-Fair-2023/ppt/pp5_presentation.pdf

2 https://calabarzon.dilg.gov.ph/dilg75-or-p8-4-billion-ayuda-distributed-to-qualified-beneficiaries-in-ncr/

3 https://business.inquirer.net/589015/philippine-gdp-growth-slows-to-2-8-in-first-quarter